Potting Profits: Best Compound Interest Investments of 2023

Nick L. · February 17, 2023 ·

Last updated

Cash doesn’t grow on trees, but compound interest is the next best thing. We looked at the top compound interest accounts to help grow your money.

Compound interest is like a superhero for your finances. It’s when the interest you earn starts earning interest, so your money just grows without you having to lift a finger.

Compound interest is like growing a money tree—every dollar you save up is a seed that grows into more money over time. The best compound interest investments are high-yield savings accounts, certificates of deposit (CDs), bonds or bond funds, money market accounts (MMAs), real estate investment trusts (REITs), and dividend-paying stocks.

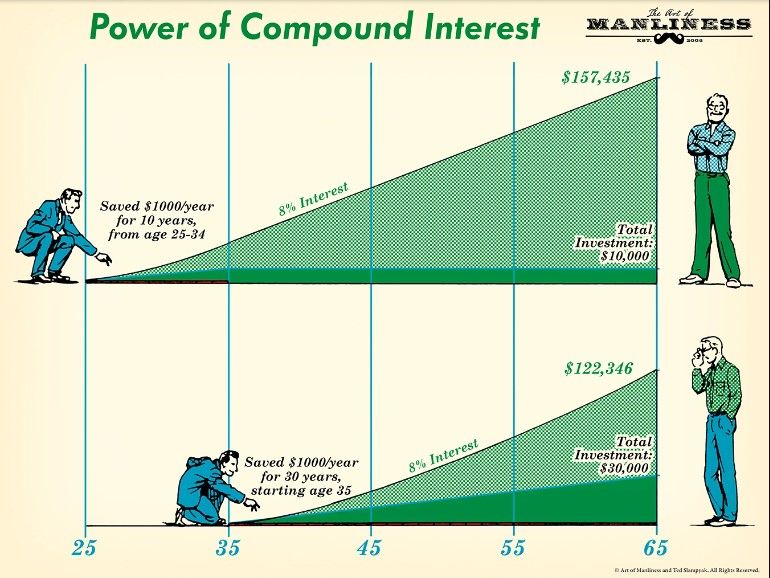

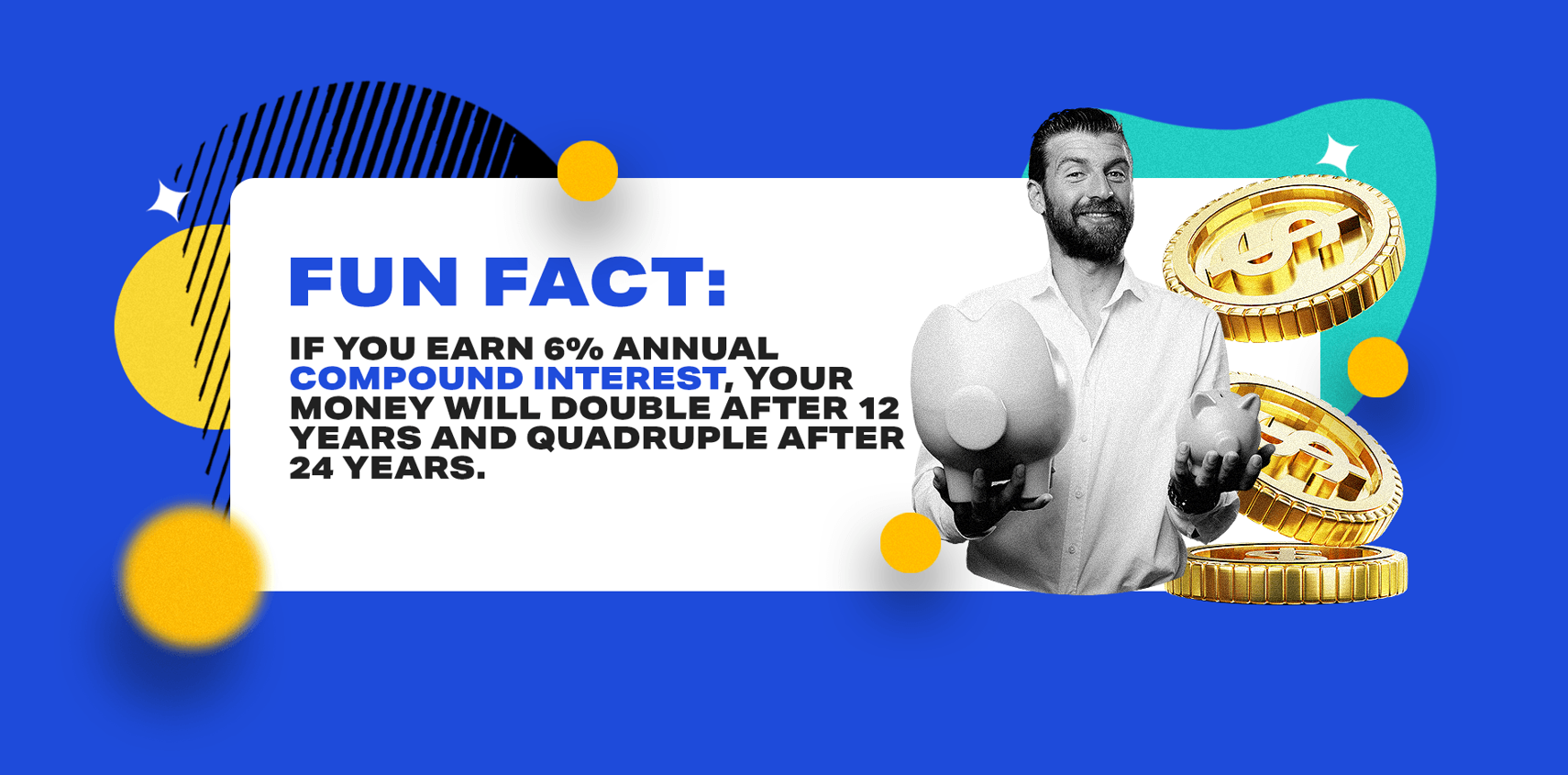

Use the ‘Rule of 72’—simply divide 72 by your expected rate of return, and you can find out how long it will take for your savings to double.

To make the most out of compound interest, it’s important to research your investments and find one that fits your needs and goals. With its profound ability to help grow your money, compound interest could be the best investment decision you ever make—and the earlier, the better.

By investing in compound interest, you’re showing patience and dedication to your financial security. In this article, we’ll talk about how you can make the most of compound interest and the best investments you can make compound interest with.

What makes compound interest investing so effective?

First, you must understand what makes compound interest investing so effective: the power of compounding. This is when your earned interest is added to your principal balance so that it earns even more interest. Over time, compounding yields higher and higher returns.

That’s why you should invest early and often—every bit of interest earned has a major impact on your balance in the long run.

Over time, compound interest creates exponential growth. For example, if you invested $1,000 for 30 years with a 5% interest rate, you would end up with almost $4,500—a huge risk-free return on your initial investment. With compound interest, even small numbers add up to big returns over the years.

Compound interest is the key to long-term wealth building, so if you’re looking to nurture a nest egg, it’s could be a fundamental part of your investment strategy. With a little bit of patience and a lot of compound interest, you may be able to retire on a private island and live like royalty. In other words, don’t waste a single day investing—take advantage of compound interest to enjoy the benefits of exponential growth.

Best compound interest investments

Compound interest investments have the power to turn even a novice investor’s money into potentially life-changing wealth. But, there’s no end-all-be-all when it comes to compound interest investments.

Whether it’s a savings account, bonds, REITs, or a dividend stock, there’s sure to be a compounding asset somewhere that’ll make your financial dreams come true. So open up your piggy banks and get started—the compound interest cash cow won’t last forever.

1. Money market accounts (MMAs)

- Average Interest Rate: 0.27% APY

- Highest Interest Rate: 4.39%

- Minimum Deposit: $0

A money market account (MMA) is one of the best compound interest investments for turning the savings of your dreams into a reality. These accounts offer interest rates ranging from a modest 0.27% to a generous 4.39%. That means more money in your pocket with less effort and practically zero risk.

MMAs are backed by the FDIC just like savings accounts, which means your balances under $250,000 are guaranteed by the U.S. government. And most MMAs don’t have a minimum balance requirement, so no need to worry about fees if you need to drain your account to buy last-minute first-class flights to Cabo.

A money market account makes it easier than ever to grow your savings. Gone are the days of measly returns on your savings account balance. With MMAs, you can take advantage of higher interest rates without tying up your cash in long-term investments or shoving it under your mattress.

You don’t even need a minimum deposit to get started. Money market accounts are one of the best ways plant the seeds of your future savings.

2. High-yield savings account

- Average Interest Rate: 3%

- Highest Interest Rate: 5.03%

- Minimum Deposit: $0

A high-yield savings account is a great place to store money in between short-term investments. These accounts can come with higher interest rates than traditional savings accounts—up to 5.03%— with similar liquidity and safety. Plus, there’s often no minimum balance required.

It’s important to note that interest rates can change—especially during economic downturns. For example, in 2020, banks adjusted their high-yield savings account interest rates several times. So keep an eye out for rate changes and banking fees, too.

High-yield savings accounts can help you put more money towards things like vacations and mortgage down payments by earning monthly returns on your money. Instead of your money sitting there and getting devalued by inflation, a high-yield savings account grows at annual average of 3%.

Plus, if you monitor your interest rates regularly, you can switch accounts to get an even better return on your money. It’s like trying to win a game of Pac-Man—you’re constantly on the hunt for the best deals so you can fill up your savings account.

Opening a high-yield savings account is a great way to make your money make money. A savings account that earns compounding yield can help you reach short-term financial goals faster by putting your money to work.

3. Mutual Funds (MFs)

- Average return rate: Up to 14.70% in the last 10 years

- Highest return rate: 32.8%

- Minimum Deposit: As low as $5

Modern mutual funds have been around since the roaring twenties and boy, have they come a long way. They were designed to pool money from multiple investors, just like how a group of people pools money to buy a gift for their friend’s birthday—except, instead of buying a gift, they buy securities (stocks, bonds, or even money market funds).

Investing doesn’t have to be as intimidating as some people make it out to be. With mutual funds, you can make investments with as little as $5 and let the professionals handle the hard stuff. Don’t worry, their track record speaks for itself. Mutual funds have been bringing in an average return of 14.70% over the past ten years, with a max return of 32.8%.

Think of mutual funds as a financial advisor doing all your investing for you. Mutual funds offer professional oversight on investments, which makes them an excellent compound interest opportunity for beginners. There might be some fees involved, but it might be worth the cost since mutual funds have proven incredibly rewarding in the long run.

4. Certificates of deposit (CDs)

- Average Interest Rate: 1.18%

- Highest Interest Rate: 4.75%

- Minimum Deposit: $0 to $500

CDs are a great way to save for a specific purpose, whether that be a down payment for a home, planning for retirement, or just being smart with your money. With CDs, you can find an interest rate that suits your needs: the average rate is 1.18%, but the best rates can fetch 4.75% annually. However, the catch is that you’ll need to make a deposit and keep there for a certain amount of time to start earning interest.

The minimum deposit amount of a CD isn’t the same across all banks. Ally Bank and Capital One offer CDs with no minimum deposit requirement, while Bank of America and Chase Bank require an initial investment of $1,000. Smaller banks, such as Marcus by Goldman Sachs and U.S. Bank, require a minimum of $500.

If you’ve got a lot of cash to spare, you can always check out jumbo CDs. These typically require a minimum deposit of $95,000, and many banks offer the same interest rate as their traditional CDs with the same terms.

Of course, you should also make sure to read the fine print, and don’t forget that sometimes, you can earn higher interest with higher minimum deposits. For example, a bank may increase the rate by 0.1% for every additional $50,000 deposited. If you’re looking to save some money with a CD, you’ll need to set financial goals, have a time horizon in mind, and compare interest rates across various banks.

5. Bonds and bond funds

- Current Interest Rate: 6.89% until April 2023

- Highest Interest Rate: 9.99% in the last 25 years

- Minimum Deposit: $1,000

Bonds and bond funds are the OG of investments—for centuries, they’ve provided a steady income stream to investors trying to offset the risks of the stock market. The most popular bonds are treasury securities, which let you lend money to the government and earn interest payments until the bond matures.

Bonds are less risky than stocks but more so than cash. The U.S. Treasury’s I-Bonds even come with a juicy 6.89% rate until April 2023—that’s pretty impressive considering the highest interest rate in the last 25 years was 9.99%. To top it off, you can get started with an initial investment of just $1,000.

Governments and businesses have always used bonds to finance their projects. You can buy treasury securities directly from the U.S. government or invest in exchange traded funds (ETFs) that hold them as underlying assets.

If you’re looking for a reliable investment, bonds and bond funds are for you. Don’t expect your savings to be launched to the moon anytime soon, but you can always count on the slow-and-steady investment strategy. Investing in treasury securities and bond ETFs is as easy as investing in the stock market—it may just be the low-risk, steady-income option you’ve been looking for.

6. Dividend stocks

- Average yield: between 2% and 5%

- Highest Yield: 4.9%

- Minimum Deposit: $0

Dividend-paying stocks have become a popular way to add an income stream to your portfolio. With the S&P 500 index typically ranging between 2% to 5% dividend yield, investors are constantly looking to capitalize on stocks that pay you to hold them.

Of course, there is always risk involved in any type of investment, and stocks are no exception. Companies that pay dividends over 8% might be on the decline, so it’s important to do your homework. This means researching their financial statements, understanding the current market conditions, and creating a well-defined investing strategy. All this helps to ensure that you don’t get blindsided.

Dividend stocks can be an excellent way to generate passive income if managed and reinvested correctly. The beauty of these stocks is that even if the value of the share goes down, you can still make money from dividends.

When it comes to investing in stocks with dividends, the critical factor is understanding the risks and opportunities associated with the company. With a little bit of due diligence and research on your stock picks, you can maximize profits and become a dividend master in no time.

7. Real estate investment trusts (REITs)

- Average Rate of Return: 13.5% in the past five years

- Highest rate of return: 39.9% in 2021

- Minimum Deposit: Starts at $1,000

Investing in REITs—or Real Estate Investment Trusts—is a great way to make money. Since 1960, when Congress first created REITs, they’ve consistently outperformed the S&P 500—with an 18.8% average annual return in revent decades. REITs also give investors the added advantage of less volatility, with some being only half as volatile as the stock market.

Basically, a REIT is a tax-advantaged company that invests in real estate. To avoid corporate tax, they’re required to pay 90% of their taxable income to investors as dividends. By law, they must invest at least 75% of their assets in real estate and generate at least 75% of their gross income from rents or mortgage interest.

REITs can be divided into two types: equity REITs and mortgage REITs. Equity REITs own a direct stake in a real asset and manage it. They collect rent and maintain the property, similar to a traditional landlord. On the other hand, mortgage REITs (mREITs) hold liabilities back by assets and use it to collect payments.

By the third quarter of 2022, mREITs paid out a massive $1.9 billion in dividends—and don’t forget, they’re earnings are tax advantaged. It’s no wonder that mREITs have become a go-to for real estate investors looking to generate passive income.

According to NAREIT data from 1994 to 2021, certain types of real estate funds come out shining. Self-storage REITs have outperformed the rest, with a total return of 18.8%. Industrial REITs have returned 15.8%, followed closely by residential (14.4%) and health care (12.7%). Office and retail subgroups both have 12.1% returns, while diversified and lodging/resorts REITs both average 9.3%. And the S&P 500? It clocks in at 10.8%.

Research shows that REITs are some of the most consistent investments out there, even in periods of rising interest rates. So if you’re looking for a steady return on investment—cash in your pocket with less volatility—then REITs are certainly worth considering.

8. Exchange traded funds (ETFs)

- Average growth rate: 10.7% annually over the last 30 years

- Highest rate of return: 245.07% in the last 5 years

- Minimum Deposit: $0

Do you wish investing was simpler? Exchange-traded funds (ETFs) may have granted your wish, no fairy godmother needed. ETFs gained tremendous popularity over the last decade and hold trillions of dollars in assets. On average, they’ve grown 10.7% annually over the past 30 years, with the highest rate of return being an unbelievable 245% in the last five years.

ETFs are like a combination of mutual funds and stocks, offering the best of both worlds. You get the diversity of mutual funds, with the ease of buying and trading stocks.

2022 was an especially wild year for the stock market, with the S&P 500 losing 19%. But if you had held any of the top ten performing ETFs, you’d have made returns between 44% to 99%. Most of these were energy ETFs, but it proves that growth can be found regardless of economic headwinds.

When you’re ready to invest, you’ll easily find an ETF to suit your budget. The median price of the most popular ETFs ranges from $3.43 to $473.56, so your minimum initial investment can vary drastically. But these days, fractional investing has made it easy to invest in high-priced stocks and ETFs without buying whole shares.

Just remember to factor in fees before pulling the trigger—ETF expense ratios are usually quite low compared to other funds, but always check to be sure. And just like that, you’re ready to start shopping around to take advantage of the awesome benefits of dividend ETFs.

Why compound interest is important

Putting your money in a compound interest investment can be a great way to double it over time. Just use the ‘Rule of 72’—divide 72 by your expected rate of return, and you can find out how long it will take for your savings to double. Let’s say your investment or savings accounts achieved a 6% return, then your money would double every 12 years.

Putting your money in compound interest accounts can be especially beneficial if you’re in it for the long haul. If you start investing early enough, and with a high enough initial amount, you might hit the jackpot (or rather the crockpot) with compound interest working its slow-cooking magic.

Think of compound interest accounts like a snowball effect—initial investments plus interest grow substantially over time. With compound interest, the longer you go, the more potential for growth. Investing early and often into you principle could mean huge gains down the line.

So, if you’re looking to make your money work for you, why not give compound interest investment a go? You could be seeing some really big returns in the future if you start early and make the most of compound interest. Who knows, you might even have enough money to buy a private island like Mr Beast.

Top Investing Platforms for collectibles

Fundrise

Real Estate

Min $104.8/5Learn more →Arrived

Real Estate

Min $1004.5/5Learn more →Ark7

Real Estate

Min $204.3/5Learn more →