Private or Public: Investing in Private Credit vs Bonds

MoneyMade Team · October 18, 2022 ·

Last updated

Investing in private credit is one popular investment strategy, but how does it hold up to other asset classes?

If following daily price movements makes you dizzy, you’re not alone. Alternative investments are on the rise, and as global markets continue to decline and interest rates rise, investors are turning away from the volatile stock market to seek uncorrelated assets for their portfolios.

The private credit market has risen dramatically in the past decade and today is nearly the size of the leveraged loan market, reaching $1.2 trillion in 2021.

Like litigation financing and blue-chip art, direct lending is a way investors can gain exposure to an alternative asset class that isn’t linked to traditional markets. But how does private credit hold up to similar investments like bonds? Get your accounting books out as we compare private credit investments with bonds to find which investment strategy is best for you.

What is private credit?

Private capital is money raised by companies to expand their business operations. It’s an asset class that includes loans and debt financed by non-banks, such as institutional investors and individual investors.

How private credit works

Small businesses, middle market companies, startups, and individuals seek private credit when they need an alternative to traditional funding sources like banks, or if they don’t have access to public markets. Private capital is often loaned to middle market firms with annual revenue of $10 million to $1 billion.

Private credit investments are illiquid, so they’re harder (if not impossible) to sell than stocks and other traditional asset types. However, many private credit offerings are short-term, so investors don’t always have to hold their investments for very long.

Risks of private credit investing

Private credit investing can be riskier than other types of investing when considering things like illiquidity, underlying credit risk, and potential exposure to market interest rates. However, the ability of a borrower to provide collateral—such as a business’s accounts receivables or equipment, or an individual’s car or property—can partially or fully mitigate credit risk.

Another way to mitigate such risks is by implementing a floating interest rate structure. If a borrower cannot repay the loan, the collateral assets can be seized to protect the lenders (AKA the investors) from potential losses.

Types of private credit

The effectiveness of private credit depends on whether it fits into your investment strategy. Private credit investment strategies can range across risk tolerance, targeted returns, asset class, and other factors. Let’s explore three subcategories of private credit and the risks and rewards that come with each one.

- venture debt

- consumer loans

- small business lending

Venture debt

Venture debt is a type of loan or financing given to help younger companies grow. Businesses often use it along with other funding methods like equity financing (selling stocks). Venture debt has unique features to accommodate companies that have not yet reached profitability, and these features may work differently than other types of loans.

For instance, venture debt is usually issued for between one and three years. While publicly-issued debt is more prominent, venture-backed companies are on the rise—on average, venture debt exceeds $30 billion annually.

Venture debt financing doesn’t always require a tangible or hard-asset collateral. Instead, lenders are compensated for providing an unsecured loan and possibly taking on more risk with things like a higher interest rate or the option to purchase equity in the borrower (AKA the company) at pre-negotiated terms.

Venture debt can be riskier than other types of investments but can have lower risk than, say, venture capital (equity investing) because lenders can include terms like collateralization and a regular payment schedule to compensate for the risk they are taking on.

Consumer loans

Consumer loans are made to individuals for personal expenditures like auto loans, personal loans, student loans, and even credit cards. These loans backed by assets are called secured consumer loans. Consumer loans require borrowers to make principal and interest payments according to its terms.

Small business lending

Small business lending is a form of private credit where small-scale businesses. These loans vary in duration, are either collateralized or unsecured, and can be used towards acquiring fixed assets—like equipment and machinery to grow a business—or to refinance other debts.

Other types of small-to-middle market business lending include cash advances and lease financing. With cash advances, companies borrow money against their future revenue in exchange for cash upfront. A cash advance relies on a company’s ability to generate revenue, not just make principal and interest payments. With small business leases, the assets are already owned by the lender, which mitigates risk by allowing the assets to be leased to a new client in the event the existing lessee defaults on its obligations.

Is private credit a good investment?

The private credit market has risen dramatically over the past decade and is nearly the size of the leveraged loan market, reaching $1.2 trillion in 2021. This was driven in part by an increased interest in private credit funds.

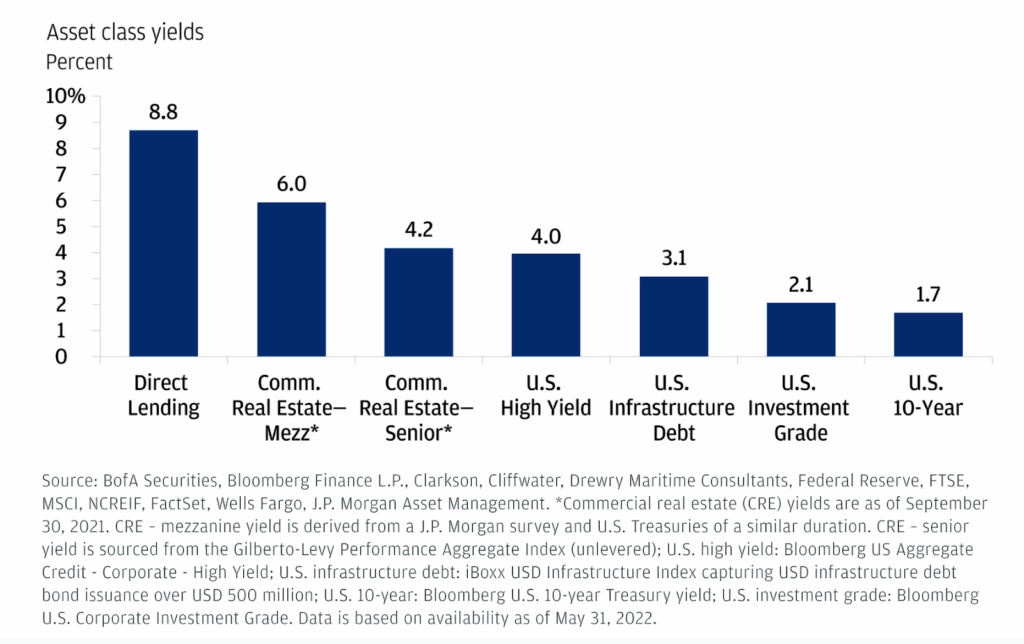

Direct lending has historically higher returns than other types of debt like commercial real estate and even bonds. On average direct lending has a return of 8.8%, making it more in line with stock market returns.

Source: jpmorgan.com

However, like any type of investment, investing in private credit has inherent risks. Besides the risk of borrowers defaulting on their loans, there’s less transparency than other types of investments like bonds or even stocks. Regulators have little control over private debt markets because they don’t have the same reporting requirements as public markets.

And with so much money in private credit markets, yields are diminishing as risk rises, leading some experts to worry about potential conflicts in the market not from other asset classes, but from other lenders.

What are bonds?

Bonds are a traditional asset class that investors hold to diversify their portfolio. Like private credit, bonds are a type of loan. But bonds are different because they can be traded on the secondary market and as exchange traded funds, although their value can fluctuate like other stocks.

Governments and corporations issue bonds to raise money. Companies might prefer to issue bonds instead of equity because it is less expensive to issue and doesn’t require giving up control of the company. By buying a bond, you’re giving the issuer a loan that they agree to pay you back at face value with interest on a specific date.

There are three general categories of bonds:

- Corporate bonds issued by private and public companies.

- Municipal bonds, sometimes referred to as munis that are issued by states, cities, counties and other types of government bodies.

- Government bonds such as U.S. Treasuries which are issued by the Treasury Department and backed by the U.S. government.

While investors can buy government or company bonds, many investors buy government bonds such as U.S. Treasuries because they are backed by the issuing country.

Are bonds a good investment?

Bonds issued by the U.S. government are considered one of the safest assets an investor can make. Bonds on the secondary market fluctuate more in price but are still considered relatively stable. The value of bonds issued by companies varies depending on their credit rating.

While U.S. Treasury bonds are safe, bond yields don’t always give promising returns. Yields on the 10-year Treasury were 3.62% as of October 5, 2022, compared to 1.49% the year before. In comparison, the stock market has historically had an average annual return of 8%. However, while stocks might have higher returns, you’re not guaranteed to get a particular return, and you could lose your money. But investors who buy and hold onto a bond until maturity are guaranteed a set return.

Investing in private credit vs. bonds

While private credit and bonds are both types of debt, private credit is riskier than investing in publicly-issued bonds. Even if you do your due diligence and a loan is secured with collateral, there are still risks. Plus, certain debt instruments are subject to interest-rate risk that may impact the long-term value of your investment.

However, private credit often yields more than government bonds to compensate for greater risk and illiquidity. As of September 30, 2022, Percent, investors have earned a historical weighted average of 12.3% APY since launching their first offering in 2019, which is double the 6.1% average annual return of bonds over the last 30 years.

Of course, past performance tells us little about what the future holds, and there’s risk with every type of investment. Rising interest rates could arguably make bonds a more attractive investment option for combating inflation as it correlates with higher yields and lower prices, but even the highest bond yields in history don’t compare to the historical returns of private market debt.

Why invest in private credit with Percent

Percent stands out as the most convenient marketplace for investing in private credit. While it’s only available to accredited investors, it’s one worth considering if you’re seeking exposure to a potentially lucrative alternative asset class. While it’s only been around since 2019, Percent has had an impressive historical weighted average return with just a 1.39% loss rate as of September 30, 2022 and a wide range of private credit investment products.

With over $714 million funded and 369 deals so far, Percent’s average investment term is just eight months, which is shorter than most other private credit products. This makes Percent more appealing to investors who want to diversify into short-term private credit without potentially locking their funds for years.

Percent also issues daily, weekly, and monthly surveillance reports to make comparing offerings and monitoring performance easier in a historically opaque asset class. While there’s no way to tell what will be the future results of the portfolio manager, Percent is great for any accredited investor looking for alternative assets to complement their traditional fixed-income portfolio.

Top Investing Platforms for stocks

Fundrise

Real Estate

Min $104.8/5Learn more →Arrived

Real Estate

Min $1004.5/5Learn more →Ark7

Real Estate

Min $204.3/5Learn more →